Pricing is one of the most important and least talked about decisions in SaaS. Most founders spend months debating their go-to-market strategy and weeks debating their hiring plan — and then set their pricing in an afternoon based on what a competitor is charging. The data shows this is more common than anyone wants to admit.

This article pulls together the most current SaaS pricing statistics available in 2026 — covering renewal price increases, the shift to usage-based models, how AI is changing pricing structures, and what the research says about which pricing approaches actually work. All data sourced from primary research published in 2025 and 2026.

Here is the full breakdown.

The Renewal Price Problem — What the Data Shows

Price Increases Are Now the Norm

The single most significant pricing story in SaaS right now is not about new customer pricing — it is about what is happening at renewal.

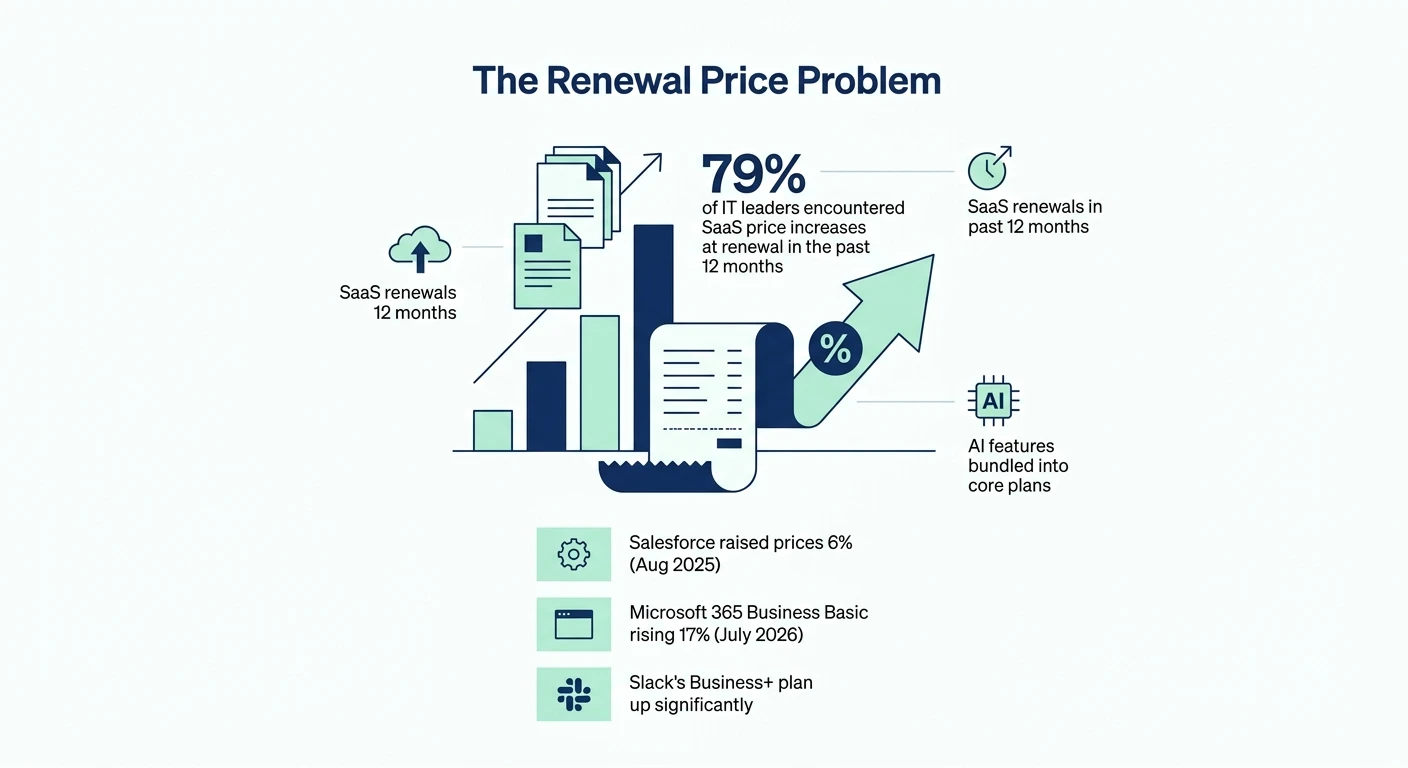

79% of IT leaders encountered SaaS price increases at renewal in the past 12 months. That is not a one-off trend driven by inflation. It reflects a structural shift in how SaaS vendors are monetizing their existing customer base — particularly as AI features get bundled into core plans and the cost of delivering those features rises.

Some real examples from 2025 and 2026:

Salesforce raised enterprise edition list prices by an average of 6% in August 2025

Microsoft 365 Business Basic is rising from $6 to $7 per user per month effective July 2026 — a 17% increase

Slack’s Business+ plan now runs $18 per user per month — up significantly from previous pricing

Across the market broadly, 73% of SaaS providers raised prices by an average of 12% between 2022 and 2023

The cumulative effect on enterprise IT budgets is significant. The average organization manages 211 SaaS renewals per year — each one now carrying a meaningful probability of a price increase that was not in the forecast model. This is why SaaS procurement has become a specialized function at larger companies rather than something that gets handled as a side task by IT.

Why Renewals Are Getting More Expensive

Three things are driving renewal price increases across the market.

AI bundling. SaaS vendors are adding AI features to existing plans and raising prices to reflect the added value — and the added compute cost. Customers who never asked for AI features and may not use them are paying for them anyway.

Market maturity. In the early days of SaaS, vendors competed aggressively on price to win market share. As categories mature and switching costs rise, the competitive pressure on pricing relaxes and vendors move prices up.

Investor pressure. Even at companies that are not burning cash, there is consistent pressure to improve net revenue retention metrics. Raising prices on existing customers is one of the fastest ways to improve NRR without acquiring new customers.

SaaS Pricing Models — What Companies Are Actually Using

The Subscription Model Still Dominates — But It Is Losing Ground

The flat monthly or annual subscription is still the most common SaaS pricing model — but the data shows it is no longer the automatic choice it once was, particularly at scale.

39% of SaaS organizations use value-based pricing — pricing based on the outcome or value delivered rather than a cost-plus or feature-based approach

24% of SaaS companies simply copy their competitors’ pricing — a surprisingly high number that suggests a lot of pricing decisions are still reactive rather than strategic

There is an almost even split between SaaS companies that publish their pricing (45%) and those that do not (55%) — though transparency is trending upward as buyers demand it earlier in the evaluation process

68% of SaaS companies discount in fewer than one-quarter of all deals — most companies maintain more pricing discipline than their sales culture might suggest

The Shift to Usage-Based and Consumption Pricing

This is the most significant structural change in SaaS pricing happening right now and the data is clear about where it is heading.

40% of SaaS companies with ARR above $50M now include consumption-based or outcome-based revenue in their ARR — compared to only 20–27% at smaller ARR bands. Usage-based pricing is a scale phenomenon — it becomes more common and more commercially important as companies grow.

Gartner predicts that by 2027, 70% of top SaaS vendors will offer consumption-based pricing for at least part of their portfolio. That is a dramatic shift from where the market was even three years ago — and AI is the primary accelerant.

The reason is straightforward. AI features have variable compute costs in a way that traditional SaaS features do not. When a customer sends a million API calls through an AI model embedded in a SaaS product, the cost to the vendor is meaningfully higher than when a customer sends a hundred. Flat subscription pricing forces the vendor to either over-charge light users or under-charge heavy ones — neither of which is sustainable at scale.

Usage-Based Pricing by ARR Band

ARR Band | % Including Consumption-Based Revenue |

Under $1M ARR | ~20% |

$1M – $10M ARR | ~23% |

$10M – $50M ARR | ~27% |

Above $50M ARR | 40% |

The pattern is consistent — the larger the company, the more likely it has moved at least part of its revenue to consumption or outcome-based models. This partly reflects the customer mix (larger companies sell more to enterprises who demand usage-based pricing) and partly reflects the pricing sophistication that comes with scale.

AI Pricing in SaaS — The New Battleground

How SaaS Companies Are Monetizing AI

Of the 41% of SaaS companies formally monetizing AI in 2026:

53% use subscription pricing for AI — bundled into existing tiers or as a dedicated AI tier

47% use usage-based, consumption, or outcome-based models for AI specifically

The subscription approach is dominant for now because it is simpler to sell, easier for customers to budget for, and easier for vendors to forecast. But usage-based AI pricing is growing fast — particularly for AI features with clear, measurable compute costs like API calls, document processing, and model inference.

The Bundling Strategy

The dominant vendor strategy in 2026 is to bundle AI features into existing plans and raise the plan price rather than offering AI as a clearly priced add-on. This approach maximizes revenue per seat but creates friction with customers who feel they are paying for features they did not request and may not use.

The data bears this out. SaaS vendors increasingly bundle AI functionality into core plans rather than offering it as optional. For buyers this means higher baseline subscription costs across the board — one of the primary drivers of the renewal price increases cited earlier.

For SaaS vendors, the bundling decision involves a genuine trade-off. Bundling AI into the base plan raises average contract value and improves NRR metrics — but it also makes pricing comparisons harder, creates perception issues with non-AI customers, and can slow deal velocity if prospects feel they are paying for something they did not ask for.

What the Research Says About SaaS Pricing Strategy

Value-Based Pricing Outperforms — But Most Companies Do Not Use It Properly

The research on pricing strategy is actually quite clear even if the execution is messy.

39% of SaaS companies use value-based pricing — tying price to the outcome or value the product delivers rather than the features it includes or what competitors charge. Companies that do this well consistently command higher average contract values and experience less price resistance in sales conversations.

The challenge is that value-based pricing requires a deep understanding of what customers actually value — and most SaaS companies have not done the quantitative customer research needed to set prices with confidence. The result is that many companies claim to use value-based pricing but are actually doing a slightly more sophisticated version of competitor-matching.

24% of SaaS companies admit to pricing by copying competitors. This is the most common bad pricing decision in SaaS — and it compounds over time because it means the entire competitive set’s pricing reflects whatever the original market entrant decided, often years ago, often based on incomplete information.

Pricing Transparency — The Buyer Expectation Gap

There is an interesting tension in SaaS pricing transparency right now.

45% of SaaS companies publish their pricing publicly. The other 55% use a “contact us for pricing” model — either because their pricing is genuinely complex and needs to be customized, or because they want the flexibility to price by deal rather than being held to a published rate.

The buyer expectation is increasingly toward transparency — particularly for SMB-focused products where buyers expect to be able to evaluate and purchase without a sales conversation. But for enterprise products, the “contact us” approach remains standard and buyers generally accept it.

Discounting Behavior

Despite the narrative that SaaS companies discount aggressively to close deals:

68% of SaaS companies discount in fewer than one-quarter of all deals

29% admit to very little discounting from their sales teams at all

The companies that discount most aggressively tend to be those with the least pricing confidence — often because they do not have a clear articulation of value that holds up under pressure. The best-performing SaaS sales teams use discounting rarely and strategically rather than as a default response to any price objection.

SaaS Pricing by Company Size

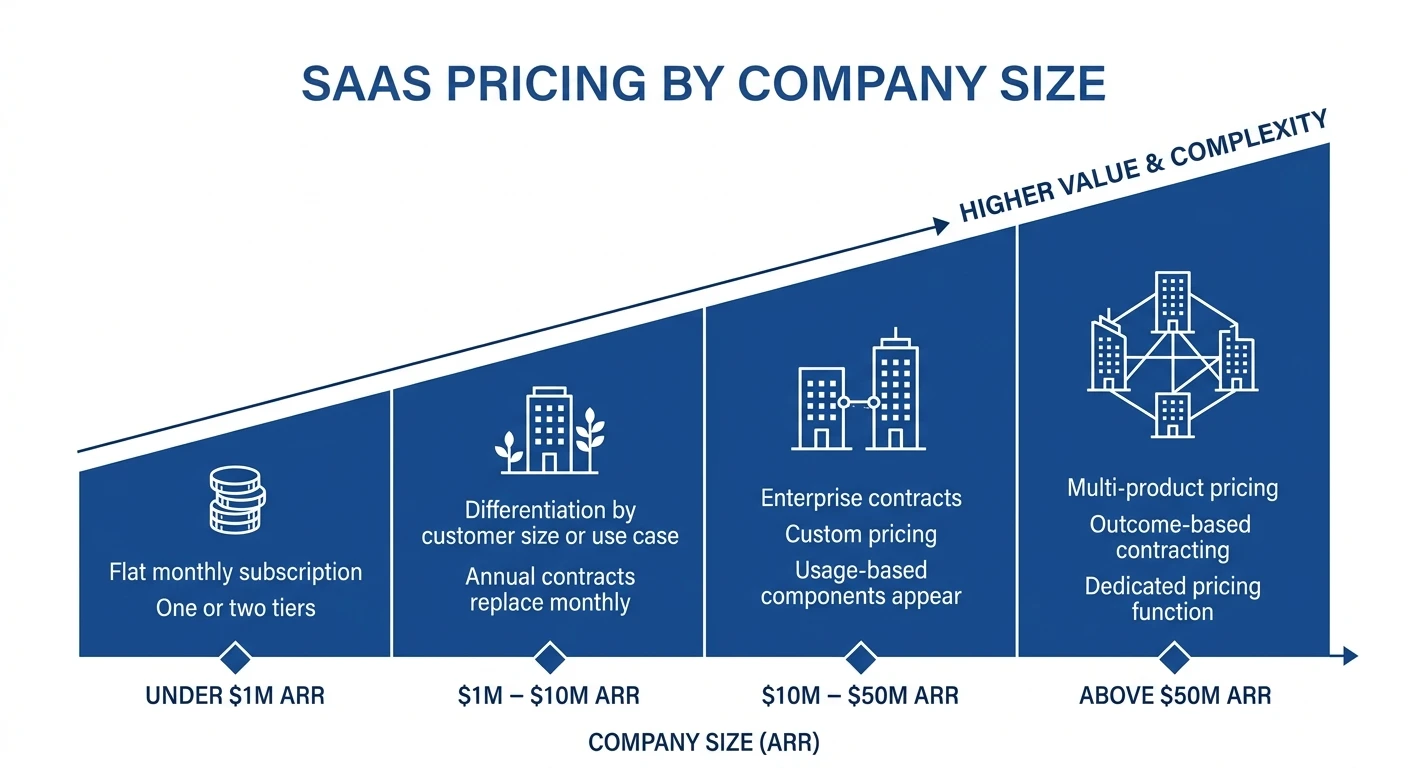

How a SaaS company prices its product tends to shift significantly as it grows. Here is what that progression typically looks like:

Under $1M ARR: Most companies at this stage are still figuring out who their ideal customer is and what they will pay. Pricing is often set too low — partly from imposter syndrome, partly from fear of losing deals. Flat monthly subscription with one or two tiers is the most common structure.

$1M – $10M ARR: Companies start to see enough customer data to understand which segments generate the most value and the lowest churn. Pricing differentiation by customer size or use case becomes more important. Annual contracts start to replace monthly.

$10M – $50M ARR: Enterprise contracts with custom pricing become a larger part of the mix. Usage-based components start to appear for higher-volume customers. The gap between the lowest and highest customer’s ACV starts to widen significantly.

Above $50M ARR: Multi-product pricing, usage-based components, and outcome-based contracting are all common. Pricing becomes a strategic function with dedicated resources rather than something handled by the CEO or head of sales.

The Pricing Metrics That Matter Most

Beyond the strategy, these are the operational pricing metrics worth tracking:

Average Contract Value (ACV): How much each customer pays on an annualized basis. Rising ACV over time (through upsells, expansion, and moving upmarket) is one of the clearest signs of pricing strategy maturity.

Price Realization Rate: The percentage of list price actually collected after discounts. Most SaaS companies track list price carefully and discount realization poorly — leading to significant revenue leakage that shows up in the financial statements but not in the CRM.

Expansion Revenue as % of New ARR: The percentage of new revenue coming from existing customers upgrading or expanding. For high-performing SaaS companies, expansion ARR represents 40% of new revenue — which means their pricing structure is actively driving growth from the existing base.

Time to First Expansion: How long it takes the average new customer to upgrade or expand their contract. Companies with strong product-led growth often see expansion happen within the first 90 days. Companies relying on human-led upsell cycles see it much later — or not at all.

Conclusion

SaaS pricing in 2026 is defined by two big forces pulling in opposite directions. Vendors are raising prices — driven by AI bundling, market maturity, and the pressure to improve NRR — while buyers are getting more sophisticated about pushing back, with dedicated procurement teams and much higher awareness of the renewal price increase problem.

The companies navigating this well are the ones with clear value-based pricing, genuine pricing transparency, and expansion mechanisms built into the product rather than bolted on by sales. The ones struggling are charging what their competitors charge, discounting to close deals, and then facing a painful renewal conversation when they try to raise prices to reflect AI feature additions.

The data on usage-based pricing tells you where this is heading. By 2027, 70% of top SaaS vendors will offer consumption-based pricing for at least part of their portfolio. The SaaS companies that start building toward that model now — even if it is just for AI features initially — will be better positioned than those that have to retrofit their entire pricing structure under competitive pressure.

We will update this article as new pricing benchmark data becomes available through 2026.

FAQs

Approximately 45-61% of SaaS companies have adopted some form of usage-based pricing, up significantly from previous years. This shift reflects growing customer demand for flexible, consumption-aligned billing rather than flat-rate subscriptions.

SaaS products with AI add-ons report renewal rates 10-20% higher than those without, as users who adopt AI features tend to become more deeply embedded in the platform. Higher engagement driven by AI tools directly correlates with stronger net revenue retention.

Seat-based pricing often fails to capture the full value delivered, especially as automation and AI reduce the number of users needed to accomplish the same tasks. Usage-based and outcome-based models allow vendors to grow revenue in line with actual customer value rather than headcount.

Yes, net revenue retention (NRR) and gross renewal rates are among the most closely watched metrics by SaaS investors, with top-performing companies maintaining NRR above 120%. A renewal rate below 80% is generally considered a warning sign of product-market fit or customer satisfaction issues.

Usage-based pricing can introduce revenue variability, but most companies mitigate this by combining it with a minimum commitment baseline or hybrid subscription model. Data shows that companies using hybrid pricing models experience more predictable revenue while still benefiting from expansion revenue tied to usage growth.

Comments

Be the first to leave a comment.