Fundraising in 2026 looks nothing like 2021. The “growth at all costs” era is definitively over. Valuations have normalised from their peak, but the companies getting funded are raising at higher multiples than ever — because investors are being far more selective about which ones they back.

SaaS still commands the largest share of venture capital of any sector. In Q3 2025, roughly 33% of all VC funding logged on Carta went to SaaS companies — the next closest was hardware at 16.5%. The global SaaS market is projected to reach $512 billion in 2026 and $908 billion by 2030 at an 18.7% CAGR. The money is still moving. It is just moving with more discipline.

Here is what the data actually shows across every stage.

Quick Reference: SaaS Funding Benchmarks 2026

Stage | Typical Round Size | Median Pre-Money Valuation | Dilution |

Pre-seed | $250K–$2M | $3M–$12M | 10–15% |

Seed | $2.5M–$5M | $14M–$24M | 12–20% |

Series A | $6M–$18M | $60M–$84M (AI: ~$84M) | 20–30% |

Series B | $20M–$50M | $80M–$160M | 15–25% |

Series C+ | $50M–$200M+ | $300M–$500M+ | Varies |

Key 2026 headline numbers:

Median seed valuation for SaaS startups: $19.8M (Carta, up from $14.7M a year prior)

Median Series A valuation: $60M (up from $44.5M in Q3 2024)

AI startups at seed command a 42% valuation premium — averaging $17.9M pre-money

AI startups at Series A hit $84M median pre-money — nearly 2x the overall median

Global software spending to reach $1.43 trillion in 2026, up 15.2% (Gartner)

SaaS funding on pace to approach $40 billion in 2026 — near 2022 levels

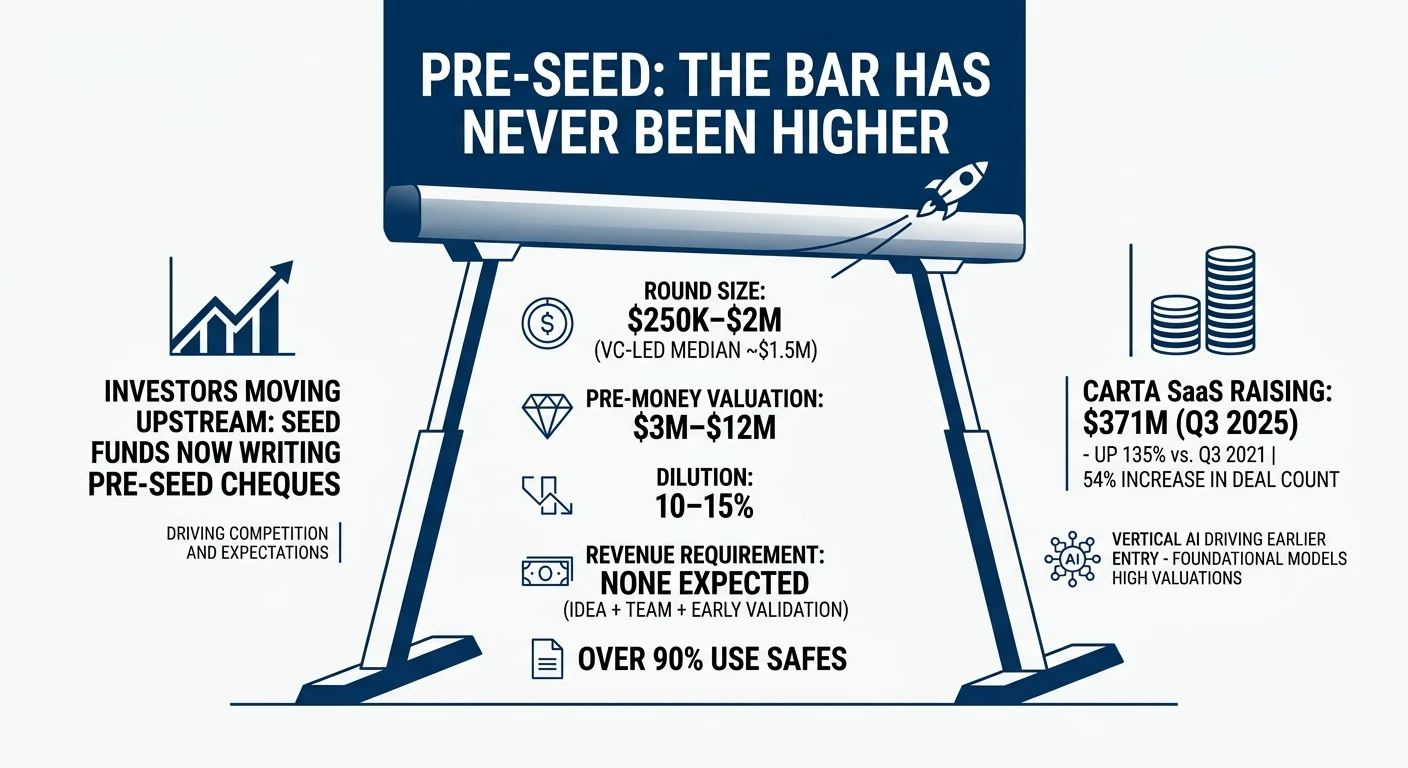

Pre-Seed: The Bar Has Never Been Higher

Pre-seed in 2026 is not what it was two years ago. Investors have moved upstream — many seed-stage funds are now writing pre-seed cheques to get in earlier, driving up both competition for deals and the expectations placed on founders.

Current pre-seed benchmarks:

Round size: $250K–$2M (angel-funded average $150K, VC-led median ~$1.5M)

Pre-money valuation: $3M–$12M

Dilution: 10–15%

Revenue requirement: None expected — idea + team + early validation

Over 90% of pre-priced rounds use SAFEs at this stage

Pre-seed SaaS startups on Carta raised $371 million in Q3 2025 — up 135% compared to Q3 2021 across a 54% increase in deal count. Investors are moving earlier, particularly in vertical AI, because foundational model companies command valuations so high that early-stage entry has become the most rational risk-adjusted position.

Seed: Valuations at All-Time Highs

The median seed round for US SaaS companies now sits at $3.1M across all industries, though the mathematical average is closer to $5.6M due to outlier AI raises. The median post-money valuation hit $24M in 2026 — an all-time high, up from $18M a year earlier.

What investors need to see at seed in 2026:

Working MVP with early validation (not just an idea)

Initial signs of product-market fit — real user adoption, consistent growth

Strong team with domain expertise or prior startup experience

ARR: $0–$1M (pre-revenue still fundable with right team and market)

Growth rate: 100–200% YoY where applicable

The seed bar has risen significantly. The $1M ARR benchmark that once qualified companies for Series A has now become a common expectation at seed for some verticals. Founders need 12–18 months of runway from seed — increasingly 24–36 months — to reduce the pressure of bridge rounds in a more selective market.

AI vs non-AI at seed: Carta now splits SaaS companies into AI and non-AI categories due to meaningfully different median valuations. AI-enhanced SaaS products command significant premiums at seed. Traditional SaaS requires stronger revenue metrics to close equivalent rounds. Over 90% of seed rounds for SaaS still use SAFEs for speed and simplicity.

Series A: The Stage Where the Metrics Bar Moved Most Dramatically

Series A is where the post-2022 correction is most visible. What qualified a company for Series A in 2019 ($1M ARR) does not come close in 2026.

Current Series A benchmarks for B2B SaaS:

ARR: $5M–$10M (up sharply from $1–$3M two years ago)

ARR growth: 100%+ year-over-year

Gross margins: 70%+

CAC payback: Under 18 months

NRR: 100%+

Round size: $6M–$18M (median ~$15M per Crunchbase)

Pre-money valuation: $60M median overall; $84M for AI-native companies

Dilution: 20–30%

The AI premium at Series A is substantial — nearly 2x the overall median. But investors are increasingly sophisticated about what “AI-native” actually means. Companies that integrate AI in a way that measurably improves retention, reduces CAC, or expands addressable capability command the premium. “AI-powered” in a slide title does not.

Many startups raising Series A in 2026 have completed multiple seed extensions or “seed-plus” rounds before reaching institutional VC metrics. The average time from seed to Series A has lengthened. Build for a 24-month seed runway if you expect to reach Series A qualification without a bridge.

Series B: Slower Activity, Larger Rounds

Series B activity declined in 2025 — total capital raised on Carta dropped 16% quarter-over-quarter and 26% year-over-year in Q3 2025. But the rounds that do close are large.

Series B benchmarks 2026:

ARR requirement: $10M+ (with $10M ARR x 8x multiple = ~$80M pre-money as a common framework)

ARR growth: 2–3x year-over-year

Round size: $20M–$50M (median ~$30M)

Pre-money valuation: $80M–$160M (peak was $160M in 2022)

Runway: 18–24 months

Revenue multiples have compressed significantly from the 2021 peak. Where SaaS companies once commanded 20–30x ARR at Series B, 2026 benchmarks cluster around 8–12x ARR for companies with strong fundamentals. Growth rate above 40% YoY commands 7–10x. Below 20% growth: 3–5x.

By Series B, investors are focused on unit economics, customer retention, and gross margin as primary valuation drivers. The narrative pitch that worked at seed does not carry at B — the numbers carry the story.

Series C and Beyond: Late Stage Takes the Largest Share

Late-stage rounds captured 68% of all North American VC funding in 2025. The biggest rounds are getting bigger while seed and early stage sees tighter competition.

Series C+ benchmarks:

Valuations: $300M–$500M+ depending on sector and growth profile

Round size: $50M–$200M+

Valuation methods: DCF models and public market comparables dominate

Pre-IPO companies valued on customer retention and gross margin as primary factors

SaaS companies growing above 40% ARR year-over-year command 7–10x ARR multiples at this stage. Below 20% growth, you are at 3–5x. The gap between high-growth and low-growth SaaS multiples has never been wider.

The AI Premium: Real, But Narrowing

Stage | AI Startup Premium vs Median |

Seed | +42% (avg $17.9M vs $12.6M) |

Series A | ~+70% (avg $84M vs ~$50M) |

Series B+ | Compressing as AI becomes standard |

The AI valuation premium is real but narrowing. As AI becomes table stakes rather than differentiator, investors are increasingly asking what the AI actually does for the business — does it improve retention? Reduce CAC? Enable a larger TAM? The companies that maintain their premium are the ones where AI is core to the product outcome, not added as a feature after product-market fit was established elsewhere.

Serial founders who have had a successful exit command 20–30% higher valuations at pre-seed and seed regardless of AI positioning. Team signal still matters enormously at early stage.

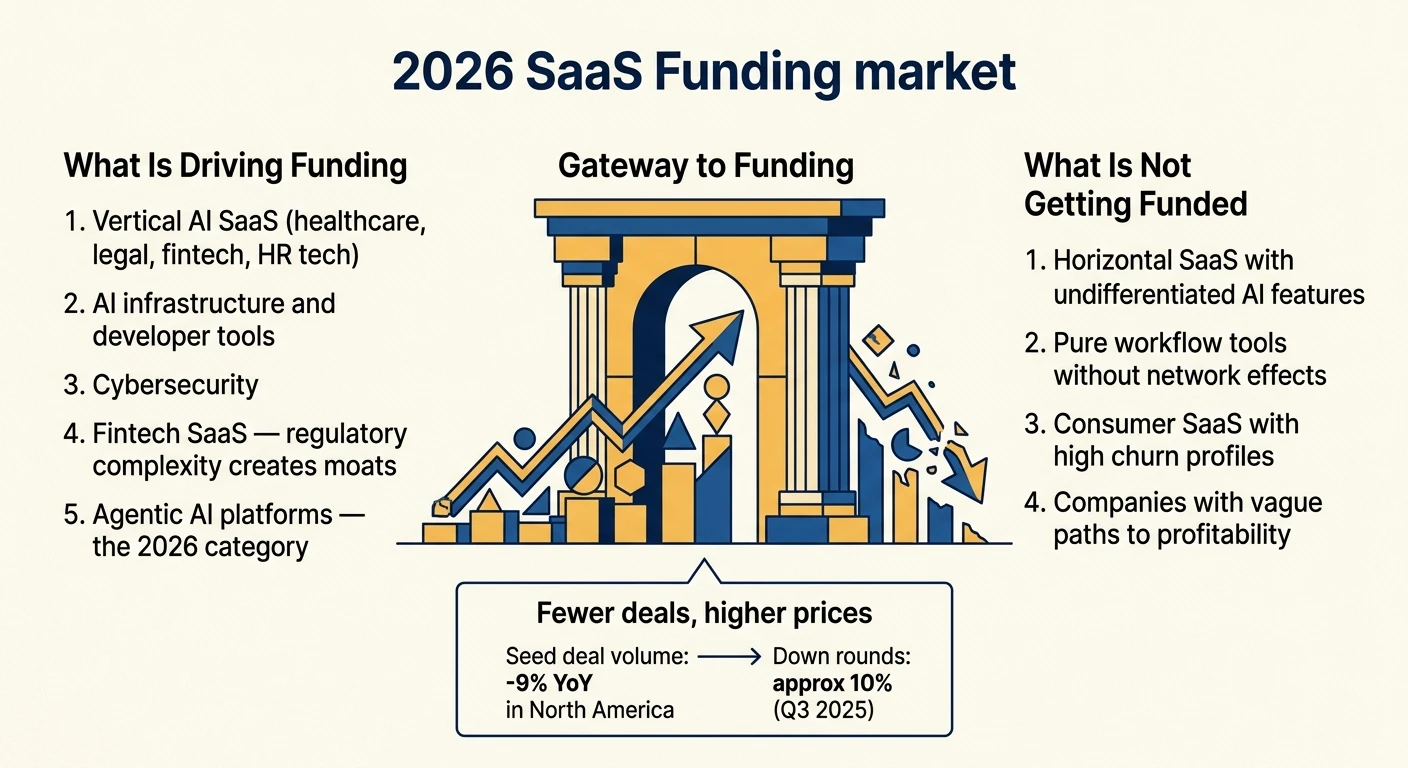

Market Context: What Is Driving Funding in 2026

The top sectors attracting SaaS investment:

Vertical AI SaaS (healthcare, legal, fintech, HR tech)

AI infrastructure and developer tools

Cybersecurity — persistent enterprise demand

Fintech SaaS — regulatory complexity creates moats

Agentic AI platforms — the 2026 category every fund wants exposure to

What is not getting funded:

Horizontal SaaS with undifferentiated AI features

Pure workflow tools without network effects or deep integration

Consumer SaaS with high churn profiles

Companies with vague paths to profitability

Fewer deals, higher prices. Seed deal volume dropped 9% year-over-year in North America even as valuations rose. Down rounds are declining — approximately 10% of rounds in Q3 2025, down from a peak above 20% in 2023. The market is stabilising but remaining selective.

What Investors Actually Want in 2026 (That They Did Not Require in 2021)

In 2021, you could raise on:

User growth

TAM narrative

Team pedigree

Vision + slide deck

In 2026, investors require:

Proven product-market fit with retention data

Clear unit economics — CAC payback under 18 months at Series A

Realistic path to profitability — not just growth

ARR metrics that match the round stage

Strong NRR (100%+ for Series A, 110%+ preferred at B)

The era of “growth at all costs” has definitively ended. The companies raising in 2026 at strong valuations are the ones that can show efficient growth — more revenue per dollar of CAC, expanding NRR, and a business model that does not require perpetual capital injection to stay alive.

FAQs

The standard expectation for a Series A in 2026 is $5M–$10M ARR, a sharp increase from the $1–$3M benchmark just two years ago. AI-focused SaaS companies with strong retention metrics can sometimes raise earlier, but the bar has risen significantly across all sectors.

Most seed rounds in 2026 target 12–20% dilution, with 15% being the common midpoint. Giving up more than 30% at seed is risky because it compresses the cap table and can create structural problems when raising later rounds.

Yes, but the premium has shrunk compared to 2024 — AI companies currently command roughly a 42% premium at seed and about 70% at Series A. Investors are increasingly demanding proof that AI is core to the product's value proposition rather than a surface-level feature addition.

Companies with strong fundamentals can typically expect 8–12x ARR at Series B, though growth rate is a major variable. Businesses growing above 40% year-over-year may see 7–10x, while those growing below 20% are often valued at just 3–5x ARR.

Overall SaaS funding in 2026 is on pace to approach the $40 billion mark last seen at the 2022 peak, signaling a genuine market recovery. However, the capital is concentrated in fewer, larger rounds, with significantly higher metric requirements at every stage, meaning fewer total companies are actually getting funded.

Comments

Be the first to leave a comment.