Churn is the number every SaaS founder watches and nobody wants to talk about honestly. The industry is full of sanitised benchmark reports that make average numbers sound almost fine. The reality is messier — and more useful if you look at it clearly.

This article pulls together the most current churn and retention data available from Recurly, ChartMogul, ProfitWell, SaaS Capital, OpenView, and Baremetrics. You will find benchmarks by company stage, customer segment, pricing model, and vertical — plus the AI-native churn story that nobody saw coming.

Quick Reference: Key SaaS Churn Statistics 2026

Metric | Number |

Average B2B SaaS monthly churn | 3.5% |

Voluntary monthly churn | 2.6% |

Involuntary monthly churn (billing failures) | 0.8–0.9% |

Median annual B2B SaaS retention | 88–90% |

Median Net Revenue Retention (NRR) | 106–110% |

Top-tier NRR | 120–130% |

Enterprise monthly churn | 0.5–1% |

SMB monthly churn | 3–7% |

Annual churn for enterprise SaaS | 5–7% |

Annual churn for SMB SaaS | 31–58% |

Involuntary churn share of total churn | 20–48% |

Recoverable involuntary churn revenue annually | $1.3 billion |

Churn reduction from switching to annual billing | 40–60% |

First 90 days as share of total annual churn | 60–70% |

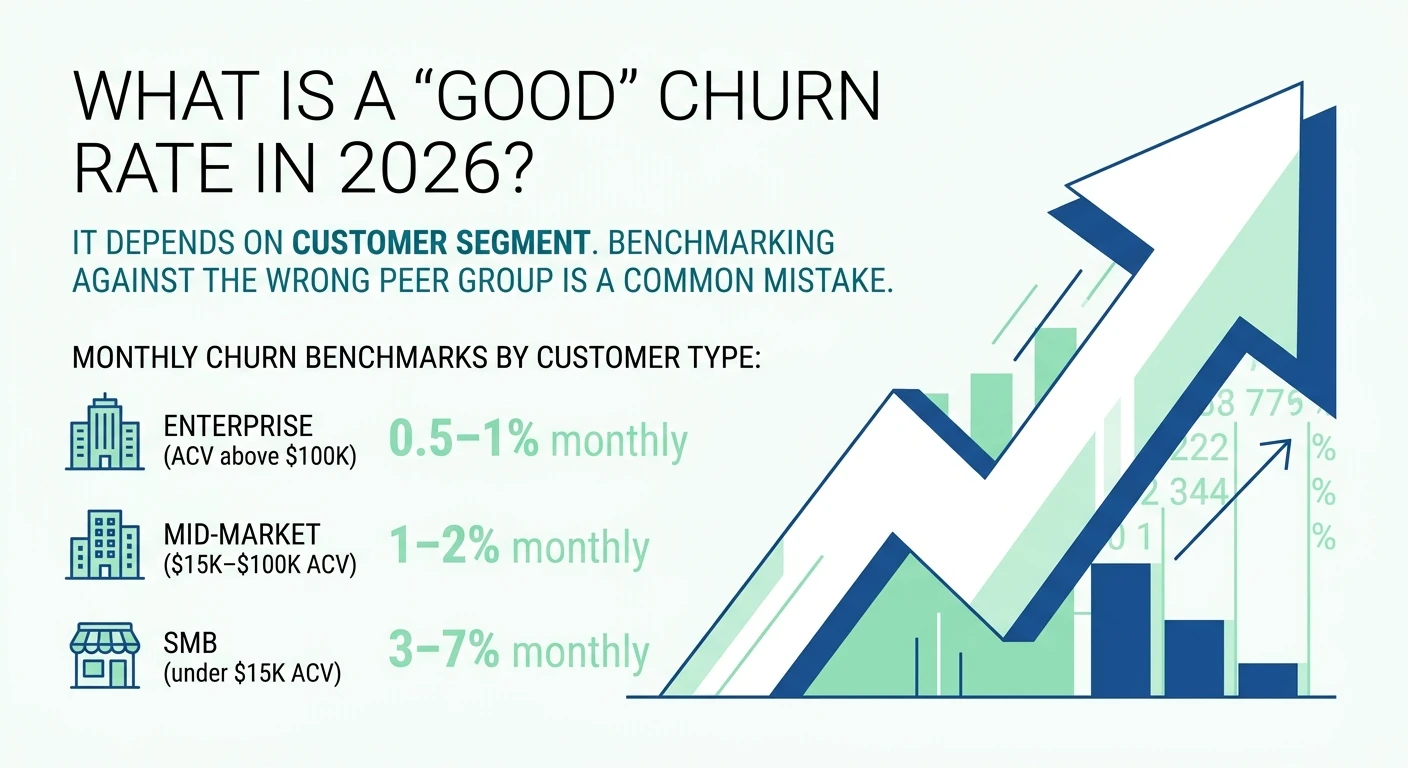

What Is a “Good” Churn Rate in 2026?

This question sounds simple. It is not. A good churn rate for a $50/month SMB tool is very different from a good rate for a $50,000/year enterprise platform. Benchmarking against the wrong peer group is one of the most common mistakes SaaS leaders make.

Here is the honest breakdown by segment:

Monthly churn benchmarks by customer type:

Enterprise (ACV above $100K): 0.5–1% monthly — target under 5% annually

Mid-market ($15K–$100K ACV): 1–2% monthly — 5–10% annually is typical

SMB (under $15K ACV): 3–7% monthly — 31–58% annually is the real range

Why the gap is so large:

Enterprise customers churn at dramatically lower rates not because enterprise products are better. It is because cancelling an enterprise contract requires executive approval, procurement involvement, data migration planning, and often 6–12 months of transition work. The structural friction suppresses churn independently of product quality. SMB customers face a completely different dynamic — higher business failure rates, more price sensitivity, and far lower switching costs.

The Census Bureau’s data on US business survival rates shows approximately 20% of employer firms exit within their first year. If your SaaS product serves early-stage businesses, you are carrying that failure rate as embedded churn risk that no retention strategy can fully overcome.

Churn Benchmarks by ARR Stage

ARR Stage | Annual Logo Churn | NRR Range |

Seed / Pre-revenue | 15–25% | 80–90% |

$1M–$5M ARR | 12–18% | 90–98% |

$5M–$10M ARR | 10–15% | 95–105% |

$10M–$30M ARR | 8–12% | 100–112% |

$30M–$100M ARR | 6–10% | 105–120% |

$100M+ ARR | 5–7% | 110–130% |

Early-stage churn looks terrifying when annualised. A 15% monthly rate at pre-revenue is actually somewhat normal — you are still figuring out your ICP, and wrong-fit customers will leave. The number that matters at early stage is whether each cohort performs better than the last. If January’s cohort retains at 65% after six months and July’s cohort retains at 75%, your product and targeting are improving. If later cohorts perform worse, something is degrading — usually sales prioritising volume over fit.

Companies over $10M ARR see 8.5% average churn. Scale brings structural retention advantages: better CS resources, longer contract terms, and deeper integrations that raise switching costs organically.

The Compounding Math That Most Founders Get Wrong

A 5% monthly churn rate does not equal 60% annual churn. Because of compounding, it actually translates to approximately 46% annual churn. Here is what different monthly rates do to a $100,000 MRR base over 12 months — assuming zero new acquisition:

Monthly Churn | 12-Month MRR Remaining | Revenue Lost |

1% | $88,636 | $11,364 |

2% | $78,500 | $21,500 |

3% | $69,384 | $30,616 |

5% | $54,036 | $45,964 |

8% | $36,770 | $63,230 |

The difference between 3% and 5% monthly churn is not a minor operational gap. On $100K MRR, it is a $15,000 monthly revenue difference that compounds into a fundamentally different business by year two.

At 2% monthly churn, a 1,000-customer base shrinks to roughly 785 customers by month 12 without any new acquisition. At 5%, that same base shrinks to around 540.

Voluntary vs Involuntary Churn: The $1.3 Billion Opportunity

Most SaaS teams focus all retention energy on voluntary churn — customers who actively decide to cancel. Involuntary churn gets less attention and represents one of the most significant recoverable revenue opportunities in SaaS.

The split:

Voluntary churn: ~2.6% monthly average (customers leaving by choice)

Involuntary churn: ~0.8–0.9% monthly (customers lost to failed payments)

Involuntary churn as share of total: 20–48% depending on segment

Involuntary churn generates approximately $1.3 billion in recoverable SaaS revenue annually. Expired credit cards alone account for 42% of all payment failures — a completely preventable churn vector that most companies address inadequately.

Smart dunning — automated retry logic, card updater services, and pre-expiry communication — recovers 50–80% of failed payments with no product changes. AI-powered payment recovery is showing 2–4x better results than traditional retry-only approaches.

The practical implication: Before you invest in a customer success hire or a new onboarding flow, fix your billing infrastructure. You are likely losing 0.5–1% of MRR monthly to payment failures that customers never even intended.

What AI-Native SaaS Churn Looks Like (And Why It Is Different)

One of the most significant churn stories of 2025–2026 is the AI-native SaaS retention crisis — and the slow recovery from it.

ChartMogul’s SaaS Retention Report data tells a striking story:

AI SaaS Segment | Gross Revenue Retention | NRR |

AI-native overall (early 2025) | 27–40% | 32–48% |

Budget AI tools (under $50/month) | 23% | 32% |

Premium AI tools (over $250/month) | 70% | 85% |

AI-native overall (September 2025) | 40% | 48% |

Traditional B2B SaaS median | 82% | 106% |

The “AI tourist” effect dominated 2025. Users signed up out of curiosity — to try ChatGPT alternatives, AI writing tools, AI image generators — with no genuine workflow need. When the novelty wore off, they cancelled. Budget-tier AI products saw 23% gross revenue retention, meaning they retained less than one in four dollars from their starting customer base after 12 months.

The good news: median GRR for AI-native SaaS climbed from 27% in January 2025 to 40% by September 2025. As tourists churn out, the remaining base is genuinely committed users who have built the tool into their workflow. The retention floor is stabilising — but it is still well below traditional SaaS benchmarks.

Premium AI tools priced above $250/month tell a completely different story — 70% GRR and 85% NRR. Higher price points attract buyers who have done proper evaluation before committing. This confirms what SaaS founders have known for years: pricing and commitment level are the strongest retention levers available, often more powerful than product improvements.

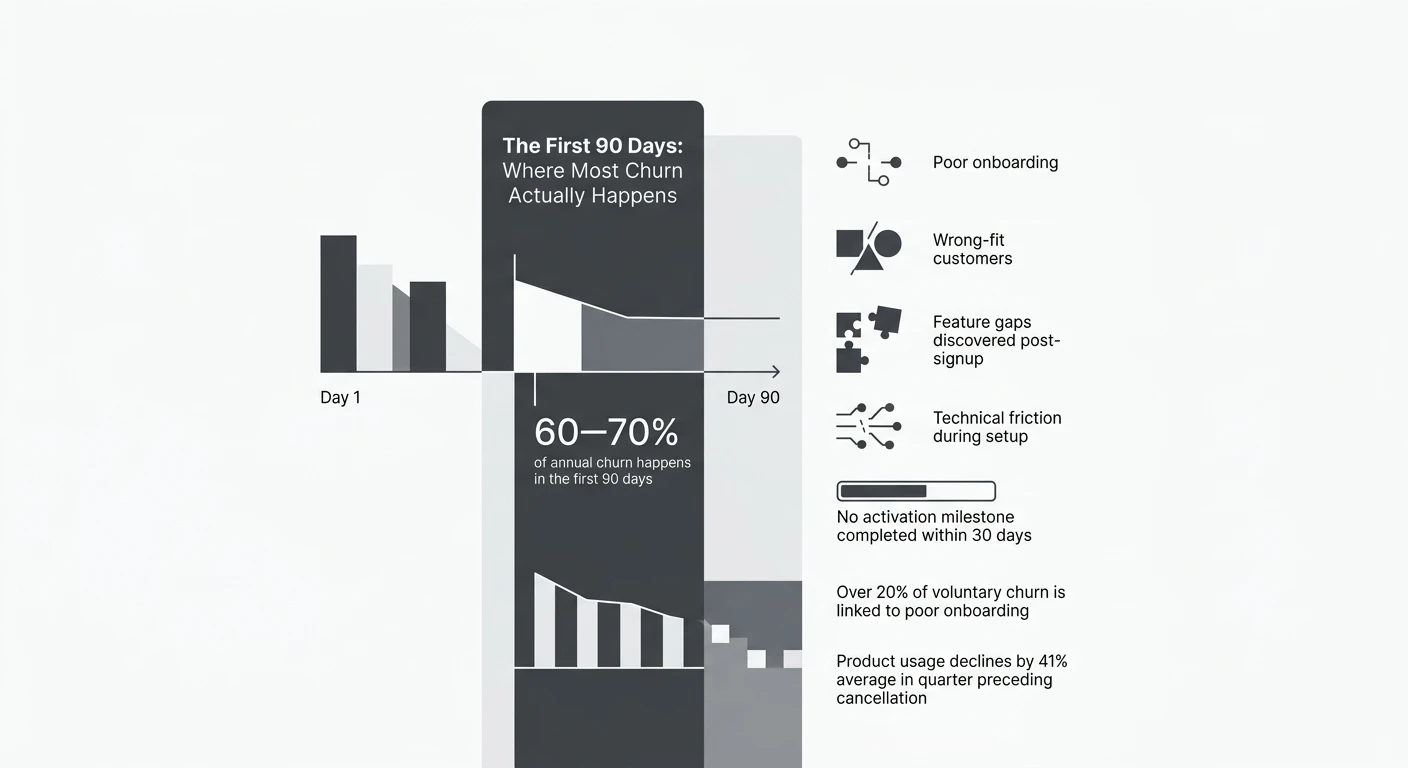

The First 90 Days: Where Most Churn Actually Happens

This is the most actionable insight in this entire article.

60–70% of annual churn happens in the first 90 days.

This is consistent across ProfitWell’s dataset and corroborated by client-level data from multiple benchmark studies. The implication is direct: if you spread your customer success resources evenly across the customer lifecycle, you are mathematically allocating the majority of your attention to the period responsible for the minority of your churn.

What happens in the first 90 days that drives churn:

Poor onboarding leaves customers unable to reach their first value moment

Wrong-fit customers who never should have been sold arrive and realise quickly

Feature gaps discovered post-signup that pre-sales glossed over

Technical friction during setup creates early abandonment

No activation milestone completed within 30 days

Over 20% of voluntary churn is directly linked to poor onboarding. Product usage declines by an average of 41% in the quarter preceding cancellation — which means the signal is detectable weeks before customers actually cancel, if usage monitoring is properly instrumented.

Pricing Model Impact on Churn

Pricing Model | Typical Monthly Churn | Notes |

Month-to-month billing | 3–8% | Continuous re-evaluation, highest churn |

Annual prepaid | 0.5–2% | Structural retention via commitment |

Usage-based | Variable | Grows with customer success |

Per-seat | 1–3% | Expansion via seat growth |

Annual subscribers churn at roughly one-third the rate of monthly subscribers across all segments. Paddle/ProfitWell data confirms this consistently. Companies that switch from monthly-default to annual-default billing — with a 15–20% discount incentive — typically cut churn by 40–60% with no product changes.

By 2026, 40% of SaaS companies with $15M–$30M in ARR have achieved negative churn through usage-based and per-seat expansion pricing models. Negative churn means the revenue gained from existing customer expansion exceeds the revenue lost to cancellations — the SaaS growth flywheel at its most powerful.

Churn by Industry Vertical

Vertical | Monthly Churn Range | Key Driver |

Healthcare IT / EHR | 0.8% | Regulatory switching costs |

Core banking / fintech | 1–2% | High integration depth |

HR tech | 1.5–3% | Annual contract norms |

Marketing tech | 2–5% | Crowded, easy to switch |

E-commerce SaaS | 3–6% | SMB customer base |

Consumer subscription apps | 6–7.5% | Discretionary spend |

AI-native tools (budget) | 7–10%+ | AI tourist effect |

Healthcare IT median monthly churn of 0.8% looks excellent. But it masks a critical risk: regulated-industry customers who decide to switch are extremely difficult to win back. The low headline rate is a lagging indicator of satisfaction — by the time a healthcare customer churns, they have been quietly unhappy for 12–18 months.

How Churn Affects Valuation

This is the number that makes investors pay attention.

The difference between 3% and 8% annual logo churn translates to a 2x–3x gap in valuation multiples for companies in the $3M–$20M ARR range

Companies with NRR above 130% trade at 15–20x forward revenue

Companies with NRR below 100% struggle to achieve 3–5x forward revenue

NRR is not just a retention metric. It is a valuation compression or expansion lever. Every percentage point of NRR improvement changes your exit multiple. For a company at $10M ARR doing a $100M exit, the difference between 105% and 115% NRR can represent tens of millions of dollars in deal value.

What Top Companies Do Differently

The companies with sub-5% annual churn share a consistent set of practices:

1. They fix involuntary churn first. Automated card updaters, smart dunning sequences, and pre-expiry communication eliminate the low-hanging fruit before investing in complex retention programmes.

2. They front-load CS resources in the first 90 days. If 65% of churn happens in the first quarter, 65% of retention investment should be concentrated there — not spread evenly across the lifecycle.

3. They use usage data as an early warning system. Product usage declining 41% in the quarter before cancellation means the signal is available weeks before the customer makes the decision. Teams with monitoring in place can intervene; teams without it are always reacting.

4. They default to annual billing. Not as an upsell — as the default. With a 15–20% discount positioned as the value, not a penalty for monthly.

5. They track NRR alongside logo churn. A company can have flat logo churn and declining revenue if their best accounts are contracting. NRR tells the real story.

FAQs

A good monthly churn rate is under 2% for SMB-focused SaaS products and under 0.5% for enterprise-focused ones. The B2B SaaS average sits at 3.5% monthly, so anything consistently above that is a signal to investigate retention issues.

Annual subscribers churn at roughly one-third the rate of monthly subscribers, making billing cadence one of the most powerful levers for reducing churn. Companies that switch from monthly-default to annual-default billing typically see churn drop by 40–60%.

AI-native tools suffer from the so-called 'AI tourist' effect, where users sign up out of curiosity rather than genuine workflow need. Budget AI tools under $50/month retained only 23% of gross revenue in 2025, while premium tools priced above $250/month retained 70–85%, indicating that price point acts as a filter for committed users.

Yes, the median NRR for B2B SaaS companies in 2026 is 106–110%, meaning expansion revenue from existing customers already outpaces losses for most well-run businesses. Top performers exceed 120% NRR, which means they can grow total revenue even with zero new customer acquisition.

Yes, if Net Revenue Retention exceeds 100%, expansion revenue from upsells, cross-sells, and usage growth more than offsets revenue lost to churn. This is why NRR is considered a more critical health metric than raw customer churn rate for scaling SaaS businesses.

Comments

Be the first to leave a comment.