The Most Anticipated IPO in Tech History

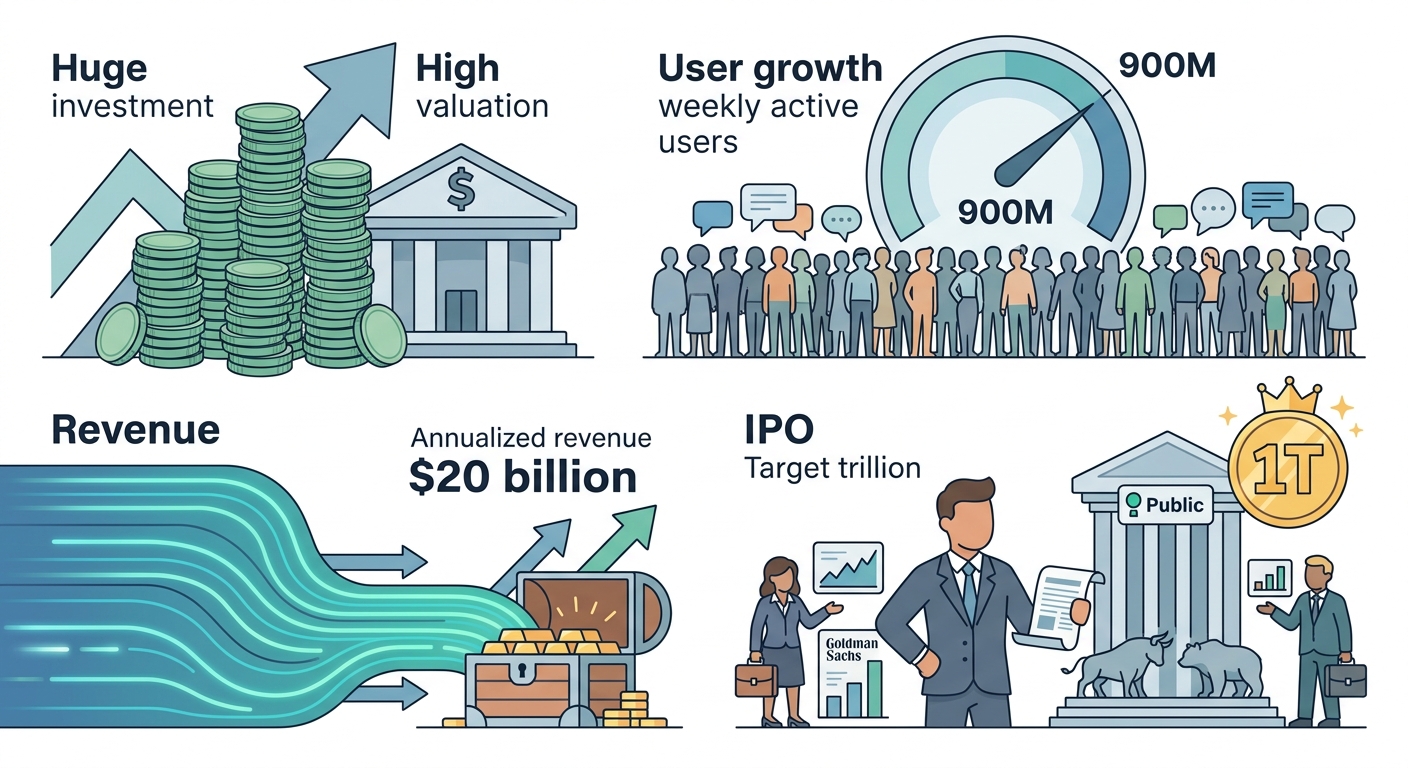

OpenAI raised $122 billion at an $852 billion valuation in its most recent funding round, with 900 million weekly active users and over $20 billion in annualised revenue.

The company is preparing to confidentially file a draft IPO prospectus, targeting a public listing as early as September 2026 at a valuation above $1 trillion, with Goldman Sachs and Morgan Stanley advising.

Those are genuinely staggering numbers. A company going from effectively zero revenue in 2022 to over $20 billion annualised in 2025 is one of the fastest revenue ramps in corporate history.

The 900 million weekly active users is a consumer platform number that rivals the largest social media companies in the world. And the $1 trillion target valuation would make the OpenAI IPO one of the largest in history by company valuation at listing.

The Problem Nobody Wants to Talk About

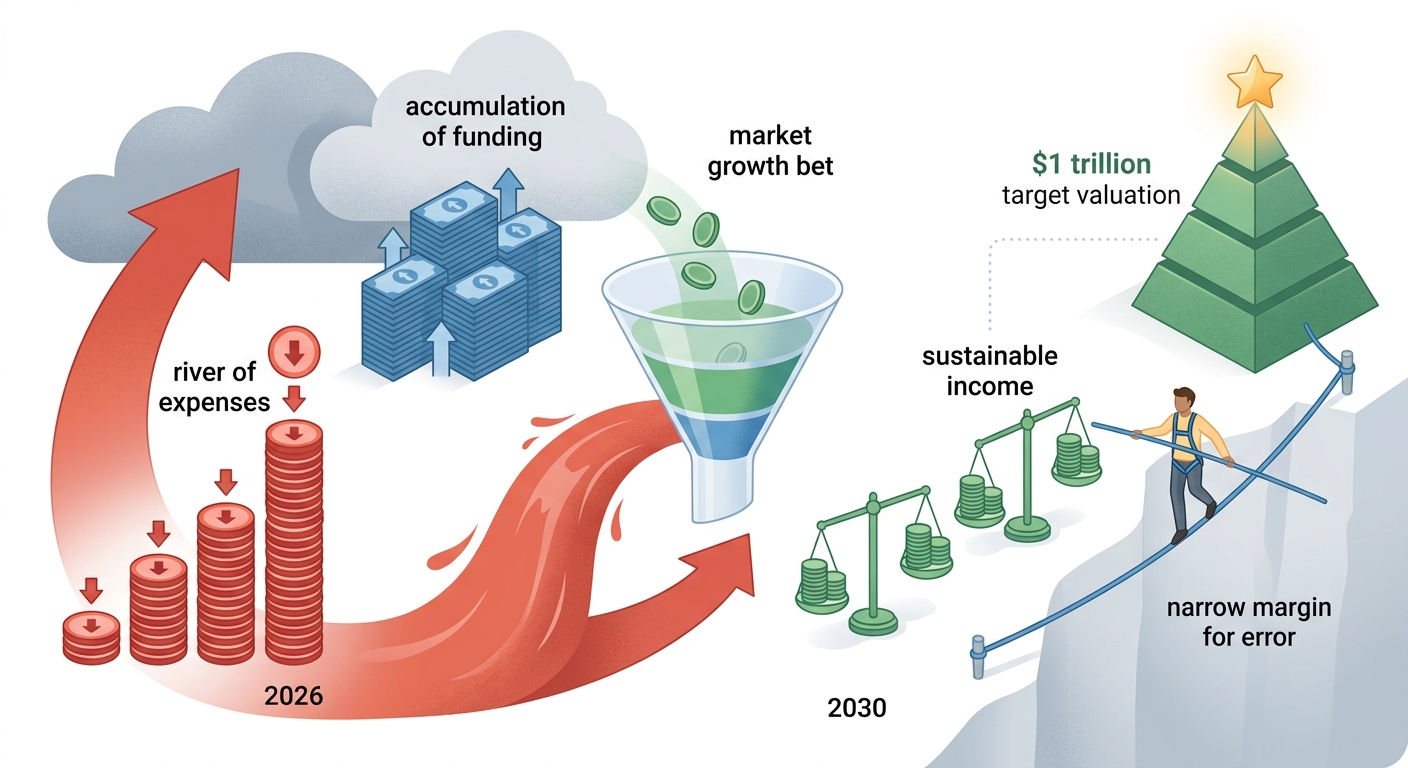

Here is the part that is not in the press release. OpenAI does not expect to reach profitability until around 2030, and internal projections suggest losses of $14 billion in 2026 alone.

HSBC analysts estimate OpenAI may need over $207 billion in additional funding before it reaches sustained profitability.

A company losing $14 billion annually while targeting a $1 trillion valuation is asking investors to make a very specific bet: that the AI market will grow large enough, fast enough, that OpenAI’s revenue will eventually catch up to its costs and produce durable profits.

That bet may well be correct. The AI market is genuinely enormous and growing fast. But it is still a bet, not a certainty — and the scale of the losses means the margin for error is narrow.

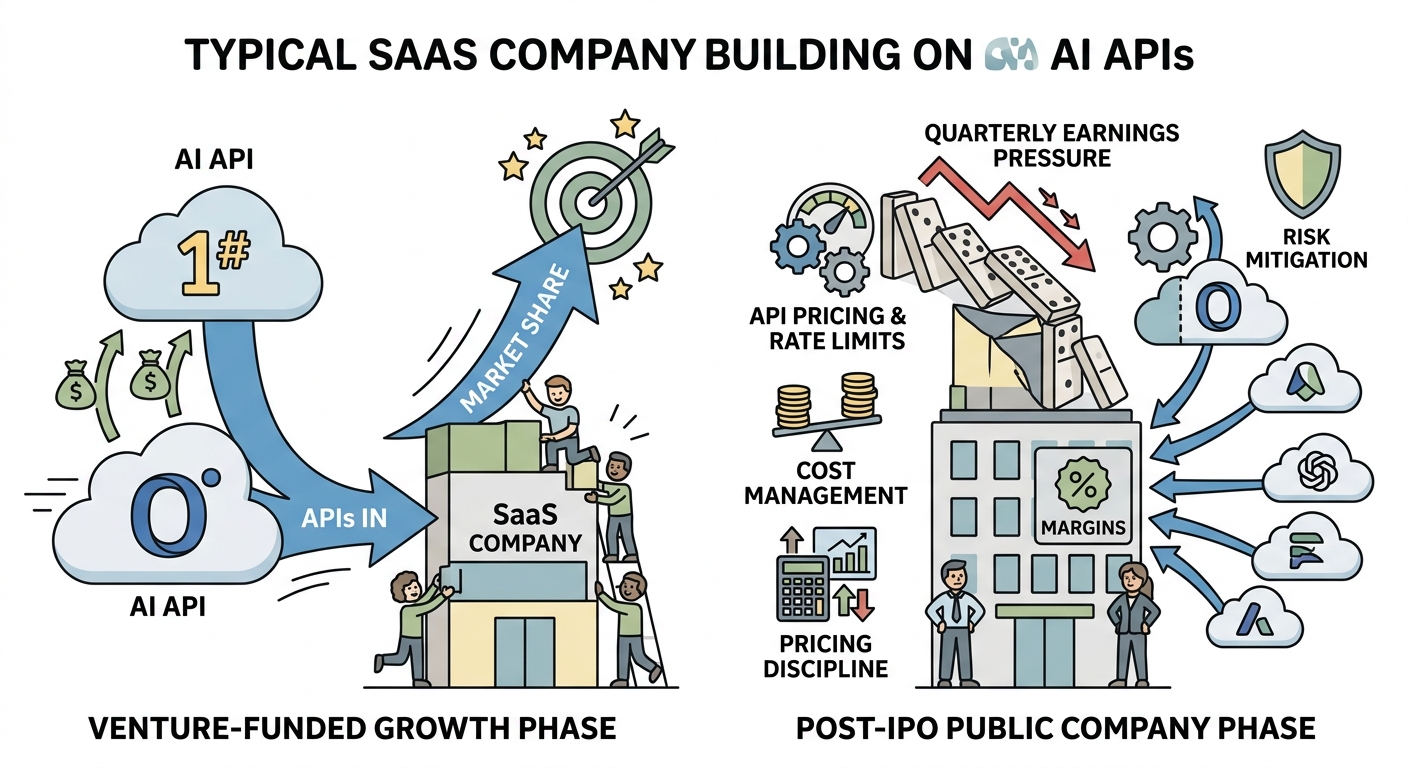

What SaaS Builders Should Watch

For SaaS companies building on OpenAI’s APIs, the IPO transition introduces specific risks worth thinking about. Public company status means quarterly earnings pressure. Quarterly earnings pressure means cost management and pricing discipline become more important than they were in the venture-funded growth phase.

API pricing, rate limits, and model availability decisions will increasingly be made with an eye on public company margins rather than purely on market share growth. Building on multiple AI providers — not just OpenAI — is sensible risk management regardless of how the IPO goes.

💬 Reddit — r/investing discussions on OpenAI IPO valuation vs losses: 🔗https://www.reddit.com/r/investing/search/?q=OpenAI+IPO+$1+trillion+valuation+losses+2026

🐦 X/Twitter — investors debating the OpenAI IPO risk-reward: 🔗https://x.com/search?q=OpenAI+IPO+trillion+valuation+2026+profitability&f=live

💬 Quora — is OpenAI worth $1 trillion given its ongoing losses: 🔗https://www.quora.com/search?q=OpenAI+IPO+worth+$1+trillion+losses+2026

Quick Links:

Comments

Be the first to leave a comment.